New vs old tax regime FY 2025-26: slabs + which saves more?

New tax regime vs old, FY 2025-26: actual numbers on which saves more between ₹7L and ₹50L CTC after Budget 2025 slabs + ₹12L rebate.

A friend pinged me last week with a Form 16 attached. He’d been on the old regime for six straight years because that’s what his TaxCalc spreadsheet inherited from his dad. He was paying ₹1.4 lakh in tax that he didn’t have to pay. Same year, same salary, new regime: zero. Not “a bit less”. Zero. He’s not unusual. He’s the median salaried filer in India right now.

Most people get this wrong by inertia. The old regime was clearly cheaper from 2020 to 2023 if you had any kind of deduction stack. Budget 2025 flipped the math for most of the salary band, and almost nobody updated their default. So you have lakhs of professionals quietly overpaying every year while their HR portal cheerfully processes whatever option got ticked back in 2020.

Here’s the short answer for FY 2025-26. Under ₹12 lakh CTC, new regime, zero tax, you don’t even need to think about it. ₹12-24 lakh, new regime usually wins by ₹50K to ₹2L a year. Above ₹24 lakh, it depends on whether you have a fresh home loan and whether you’re in a metro paying real rent. That’s the whole piece in three sentences. The rest is the math to prove it for your specific salary.

What Budget 2025 actually did

The Finance Minister reshuffled the new-regime slabs and widened the Section 87A rebate in the February 2025 budget. The 5% bracket now starts at ₹4 lakh instead of ₹3 lakh. A new 25% slab appeared between ₹20 lakh and ₹24 lakh, breaking what used to be a brutal jump from 20% to 30%. And the rebate was bumped so that any taxable income up to ₹12 lakh under the new regime comes out to zero tax. Standard deduction stayed at ₹75,000, which means the rebate effectively shields gross salary up to ₹12.75 lakh.

The old regime got nothing. Same slabs as 2014. Same ₹50,000 standard deduction. Same ₹2 lakh Section 24(b) cap. All your deductions still work (80C, 80D, HRA, the lot), they just work on a tax base that the new regime now beats at almost every salary point. Translation: the gap between what the old regime can save you and what the new regime starts you at has been closing for five years straight, and Budget 2025 closed it the rest of the way for most filers.

The slab tables you actually need

New regime, FY 2025-26 (AY 2026-27):

| Taxable income (after ₹75K standard deduction) | Rate |

|---|---|

| Up to ₹4,00,000 | Nil |

| ₹4,00,001 to ₹8,00,000 | 5% |

| ₹8,00,001 to ₹12,00,000 | 10% |

| ₹12,00,001 to ₹16,00,000 | 15% |

| ₹16,00,001 to ₹20,00,000 | 20% |

| ₹20,00,001 to ₹24,00,000 | 25% |

| Above ₹24,00,000 | 30% |

Section 87A rebate under the new regime: full rebate up to ₹12 lakh taxable income, capped at ₹60,000.

Old regime, the same since 2014:

| Taxable income (after ₹50K standard deduction + all other deductions) | Rate |

|---|---|

| Up to ₹2,50,000 | Nil |

| ₹2,50,001 to ₹5,00,000 | 5% |

| ₹5,00,001 to ₹10,00,000 | 20% |

| Above ₹10,00,000 | 30% |

Section 87A rebate under the old regime is stuck at the ₹5 lakh ceiling with a ₹12,500 cap. Both regimes add 4% Health and Education Cess on the final tax figure. Surcharge kicks in above ₹50 lakh.

The ₹12 lakh rebate trick

This is the change that did all the work, and most people I talk to still don’t quite believe it. Up to ₹12 lakh taxable income under the new regime, your tax is zero. Not “low”. Zero rupees.

The mechanics. Compute slab tax the usual way. At exactly ₹12 lakh taxable, slab tax is ₹60,000. Then Section 87A says: rebate equals the tax payable, capped at ₹60,000, for incomes up to ₹12 lakh. So the rebate cancels the ₹60,000. Then you add 4% cess on what’s left, which is zero. Total: zero.

Cross ₹12 lakh by even one rupee and you might think you suddenly owe ₹60,000 plus the marginal slab tax. You don’t. The Act provides marginal relief between roughly ₹12 lakh and ₹12.75 lakh: your tax cannot exceed the income above ₹12 lakh. So at ₹12.5 lakh taxable, you owe about ₹50,000 of tax (the additional income), not the ₹66,500 the slab tables would suggest. After ₹12.75 lakh-ish, you cross over to the normal slab math. The cliff people are afraid of is actually a gentle ramp. Walk it.

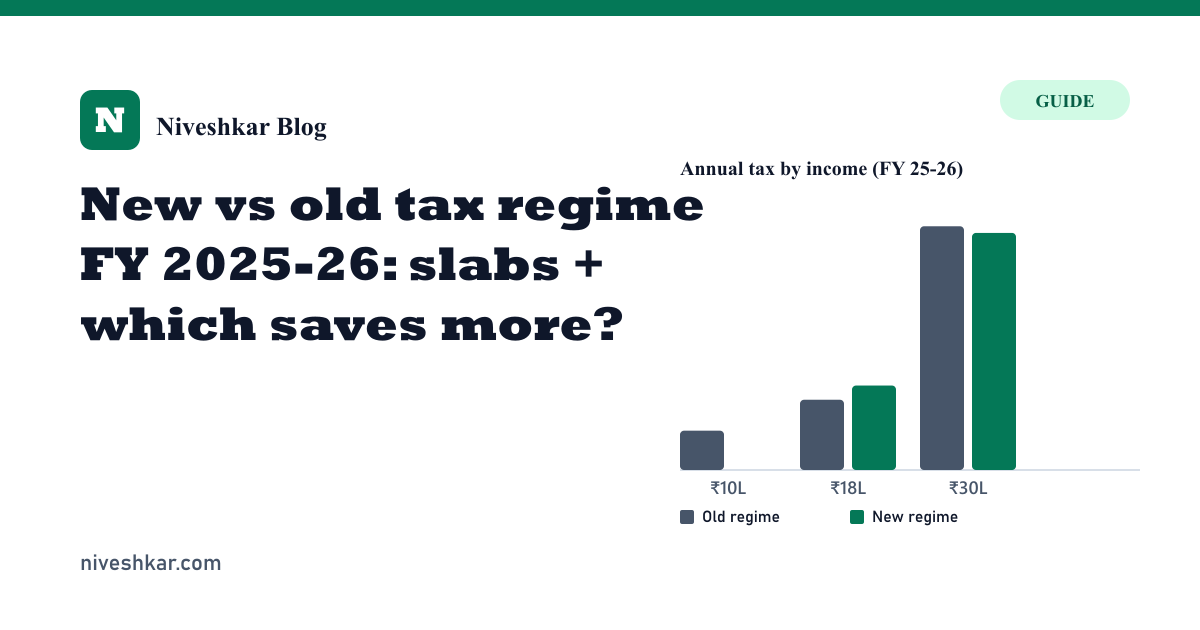

Worked example: ₹10 lakh CTC

Single, mid-twenties, living with parents in Pune. EPF deducted on a basic of ₹4 lakh, so ₹48,000 a year flowing in there. No home loan, no HRA claim because parents aren’t going to suddenly start charging rent.

Under the new regime, standard deduction of ₹75,000 brings taxable income to ₹9,25,000. Slab tax: 5% on ₹4-8 lakh (₹20,000) plus 10% on ₹8-9.25 lakh (₹12,500). That’s ₹32,500 of slab tax. Section 87A rebate is ₹32,500 because taxable income is well under ₹12 lakh. Net tax: zero.

Under the old regime, standard deduction is only ₹50,000. Then 80C up to ₹1.5 lakh (EPF ₹48,000 + ₹52,000 ELSS + ₹50,000 PPF, exactly hitting the cap). 80D health insurance ₹25,000. No HRA. Taxable income: ₹10,00,000 − ₹50,000 − ₹1,50,000 − ₹25,000 = ₹7,75,000. Slab tax: ₹12,500 (5% on 2.5-5L) + ₹55,000 (20% on 5-7.75L) = ₹67,500. Rebate doesn’t apply because taxable income is over ₹5 lakh. Cess 4% = ₹2,700. Net tax: ₹70,200.

New regime wins by ₹70,200. Nothing closes that gap at this income. No deduction stack you can plausibly build will make the old regime competitive here. If you’re under ₹12 lakh CTC and you’re still ticking the old regime box on your declaration form, you’re voluntarily paying ₹50,000 to ₹80,000 a year to the government for no reason.

Worked example: ₹18 lakh CTC

The interesting income band. Year-3 software engineer, basic ₹7.2 lakh, HRA component ₹3.6 lakh in CTC. Renting in Bangalore at ₹35,000/month, so ₹4.2 lakh of actual rent paid. Home loan of ₹40 lakh outstanding at 9%, year-1 interest about ₹3.55 lakh. EPF at 12% of basic = ₹86,400.

New regime first because it’s simpler. Standard deduction ₹75,000. Taxable income: ₹17,25,000. Slab tax: ₹20,000 (5% on 4-8L) + ₹40,000 (10% on 8-12L) + ₹60,000 (15% on 12-16L) + ₹25,000 (20% on 16-17.25L) = ₹1,45,000. No rebate above ₹12 lakh taxable. Cess 4% = ₹5,800. Net tax: ₹1,50,800.

Old regime needs more work. Standard deduction ₹50,000. HRA exempt under Section 10(13A) is the minimum of three numbers: actual HRA received (₹3.6L), rent minus 10% of basic (₹4.2L − ₹72K = ₹3.48L), and 40% of basic (₹2.88L). Note the 40%, not 50%: Bangalore is not a metro for HRA, only Delhi, Mumbai, Kolkata and Chennai are, a point the HRA exemption guide digs into. Lowest of the three is ₹2.88L, so that’s the HRA exemption. Then 80C ₹1.5L (EPF ₹86,400 + a ₹63,600 ELSS top-up). 80D ₹25,000. Section 24(b) home loan interest ₹2 lakh, capped. Taxable income: ₹18L − ₹50K − ₹2.88L − ₹1.5L − ₹25K − ₹2L = ₹10.87L. Slab tax: ₹12,500 + ₹1,00,000 + ₹26,100 (30% on the ₹87K above ₹10L) = ₹1,38,600. Cess 4% = ₹5,544. Net tax: ₹1,44,144.

Old regime wins, but only by ₹6,656. This is the income band where the answer isn’t obvious, and the margin here is thin enough that a single changed assumption flips it. Strip out the home loan (sell the flat, move to renting only) and the new regime takes back the lead by about ₹56,000. The deciding factor is Section 24(b). If you have it and you’re using the full ₹2 lakh cap, old regime is probably still ahead. If your loan has aged past year 7 and interest has dropped below ₹2 lakh, recheck because the shield is shrinking and the answer flips back. Run the EMI calculator on your actual outstanding balance to see what your year-by-year interest looks like.

Worked example: ₹30 lakh CTC

Mid-career manager. Basic ₹12 lakh. HRA component ₹6 lakh. Renting in Mumbai at ₹50,000/month = ₹6 lakh/year. Home loan year-1 interest ₹4.8 lakh (₹60 lakh outstanding at 8%). EPF ₹1.44 lakh. Employer NPS contribution at 12% of basic = ₹1.44 lakh.

New regime. Standard deduction ₹75,000 plus the ₹1.44 lakh employer NPS contribution (Section 80CCD(2) is allowed in the new regime up to 14% of basic, so the full amount goes through). Taxable income: ₹30L − ₹75K − ₹1.44L = ₹27.81L. Slab tax: ₹20,000 + ₹40,000 + ₹60,000 + ₹80,000 + ₹1,00,000 + ₹1,14,300 (30% on the ₹3.81L above ₹24L) = ₹4,14,300. Cess 4% = ₹16,572. Net tax: ₹4,30,872.

Old regime. Standard deduction ₹50,000. HRA exempt = min(₹6L, ₹6L − ₹1.2L = ₹4.8L, 50% of ₹12L = ₹6L) = ₹4.8L. 80C ₹1.5L. 80CCD(1B) NPS ₹50,000 extra. 80D ₹50,000 (self + senior parents). Section 24(b) ₹2L. Taxable income: ₹30L − ₹50K − ₹4.8L − ₹1.5L − ₹50K − ₹50K − ₹2L = ₹20.2L. Slab tax: ₹12,500 + ₹1,00,000 + ₹3,06,000 (30% on ₹10.2L above ₹10L) = ₹4,18,500. Cess 4% = ₹16,740. Net tax: ₹4,35,240.

New regime wins by ₹4,368 here, even with the kitchen-sink deduction stack. The margin is narrow, which is why this is the income band where personal finance Twitter spends most of its time arguing about. Strip the home loan out and the new regime advantage jumps to about ₹70,000. The trajectory is clear: every year you delay deciding, the new regime gets a bit fatter and the old regime stays exactly where it was in 2014.

When the old regime still wins

A short list. Read it and check if you fit.

Home loan in years 1 to 5 of tenure with interest still maxing the ₹2 lakh Section 24(b) cap, AND living in rented accommodation in a metro paying ₹40,000 or more in monthly rent. This is the one combination the new regime can’t touch. Section 24(b) plus full HRA is worth ₹5.5-6.5 lakh of deductions before you’ve even started on 80C.

Parent with a major health expense in the year. Section 80DDB for specified diseases (cancer, neurological disorders, chronic kidney disease) allows ₹40,000-₹1 lakh of deduction depending on senior-citizen status. Stack this on top of normal 80D and the deduction pile shoves you past where the new regime can compete.

Consultant filing under ITR-4 with presumptive 44ADA at 50% margin, AND holding a home loan, AND a dependent parent on health support. The triple combination of 24(b) + 80C + 80D + 80DDB can stack into the ₹7-8 lakh deduction zone where even the FY26 new regime can’t catch up. This is a narrow demographic, but the people in it know who they are.

Outside these three situations, the new regime wins from ₹7 lakh CTC to about ₹40 lakh CTC for almost every salaried profile. Above ₹40 lakh, depends. Below ₹40 lakh without one of the three triggers above, just tick new.

The math to run in five minutes

Sit with two columns and a calculator. Compute taxable income under each regime separately. Apply each slab table. Apply the rebate where it qualifies. Add 4% cess. Take the lower one and tick it on your ITR. Or skip the columns entirely and run your salary through the income tax calculator, which does both regimes side by side and hands you the monthly take-home too.

The income tax department’s e-filing portal does this automatically once Form 16 is uploaded, but the recommendation it shows can be wrong if your deductions aren’t entered properly. Don’t trust the portal’s default if you have any kind of deduction stack. Compute it yourself first.

The choice is per-financial-year for salaried filers, so you can switch annually without consequences. One exception: if you have business income filing under ITR-3 or ITR-4 and you opt out of the new regime, you cannot opt back in. Most ITR-1 and ITR-2 filers don’t hit this lock and can flip as often as the math says to flip.

The TDS thing that costs people money

Plenty of companies still default new joiners to the old regime in their April payroll declaration form because the form is old and HR hasn’t updated it. If the new regime is cheaper for you, declare it to HR in April so monthly TDS is computed against the lower regime. Skip this and you’ll get a fat refund in August-October, which is fine for cashflow if you have surplus, but expensive otherwise.

A ₹1 lakh of advance TDS sitting with the government for ten months instead of in your account is about ₹5,000 of opportunity cost at expected equity mutual fund returns. Drop it into a SIP instead and that ₹5,000 a year compounds over a career into something that buys at least one extra month of post-retirement expenses. Worth fixing in April rather than chasing a refund six months later.

Habit is the enemy of net pay

I’ll tell you what my friend with the wrong-regime Form 16 said when I showed him the alternative number. He said “but my CA always did old regime”. The CA hadn’t run the comparison since 2023. The CA was charging ₹3,000 a year. The CA was costing him ₹1.4 lakh a year.

Run your own numbers. The slab changes from Budget 2025 mean the answer for at least 60% of salaried filers in India this filing season is the new regime, even when their existing setup has been the old regime for a decade. The portal won’t tell you to switch. Your CA might not have re-run the comparison. The default option is whatever you ticked last year. Inertia is the most expensive line item on the average Indian salary slip right now.