HRA exemption calculation: the Section 10(13A) three-way minimum explained

HRA exemption calculation made simple: the Section 10(13A) three-way minimum, metro vs non-metro, rent to parents, and why the new regime kills it.

A colleague in Bengaluru claimed HRA at 50% of his basic for three years running. He thought Bengaluru was a metro. It isn’t, not for HRA, and when his return got picked for a routine check, the assessing officer wanted an explanation for the gap. He got lucky: the rent leg was actually the binding one in his case, so the final exempt figure didn’t change and the mismatch was waved through. Most people aren’t that lucky. The metro myth is the single most common HRA mistake I see, and it’s entirely avoidable once you know the four-city list.

Here’s the whole thing in one line. Your exempt HRA is the lowest of three numbers: the actual HRA your employer pays, your rent minus 10% of basic, and 50% of basic if you’re in Delhi, Mumbai, Kolkata or Chennai (40% everywhere else). The rest of this piece is just showing you which of the three usually bites, and the edge cases that trip people up. If you’d rather skip the arithmetic, run your figures through the HRA calculator first and come back for the reasoning.

The Section 10(13A) formula

Section 10(13A) of the Income Tax Act, read with Rule 2A of the rules, is the law that lets a salaried person keep part of their HRA tax-free. The exempt amount is the minimum of three figures, all computed for the financial year:

- The actual HRA your employer pays you.

- Rent paid minus 10% of basic salary (add DA if it forms part of retirement benefits).

- 50% of basic if you live in a metro, 40% if you don’t.

Take the smallest. That’s exempt. Whatever HRA you receive above that figure is taxable salary, added to your income and taxed at your slab.

Two things worth nailing down before any example. The formula runs on basic salary, not on gross or CTC. If your basic is a thin slice of a fat package, all three legs shrink, and your exemption is smaller than your rent might lead you to expect. And the second leg, rent minus 10% of basic, is the one that quietly does the capping for most renters. People stare at the HRA line on their payslip, assume it’s all tax-free, and forget the rent leg exists.

Metro vs non-metro: only four cities count

This is where the money leaks. For HRA, “metro” means exactly four cities: Delhi, Mumbai, Kolkata and Chennai. That’s it. The list hasn’t grown to match the country’s actual urban map. Bengaluru, Hyderabad, Pune, Gurugram, Noida, Ahmedabad, all of them are non-metro for HRA, so the third leg is 40% of basic, not 50%.

The gap is 10% of your annual basic. On a ₹6 lakh basic, that’s ₹60,000 of potential exemption riding on whether you tick metro or not. Now, in plenty of cases it doesn’t change the final answer, because the rent leg is lower than both percentage legs anyway. But where the percentage leg is the binding one, claiming a metro status you don’t have is a clean, checkable error. The department has your address. Don’t hand them a mismatch for the sake of a leg that often wasn’t going to help.

Worked example: Mumbai, the clean case

Monthly basic ₹50,000, HRA ₹20,000, rent ₹25,000, living in Mumbai. Annualise everything and run the three legs.

Actual HRA: ₹2,40,000. Rent for the year is ₹3,00,000, minus 10% of the ₹6,00,000 basic (₹60,000), so ₹2,40,000. Metro leg: 50% of ₹6,00,000, so ₹3,00,000.

The three numbers are ₹2,40,000, ₹2,40,000 and ₹3,00,000. Lowest is ₹2,40,000, and here both the actual-HRA leg and the rent leg land on it. So the full ₹2,40,000 of HRA is exempt, nothing is taxable. At a 20.8% marginal slab, that’s roughly ₹49,900 of tax you don’t pay. This is the case everyone hopes for: the HRA component lines up with what the formula allows, so none of it spills into taxable salary.

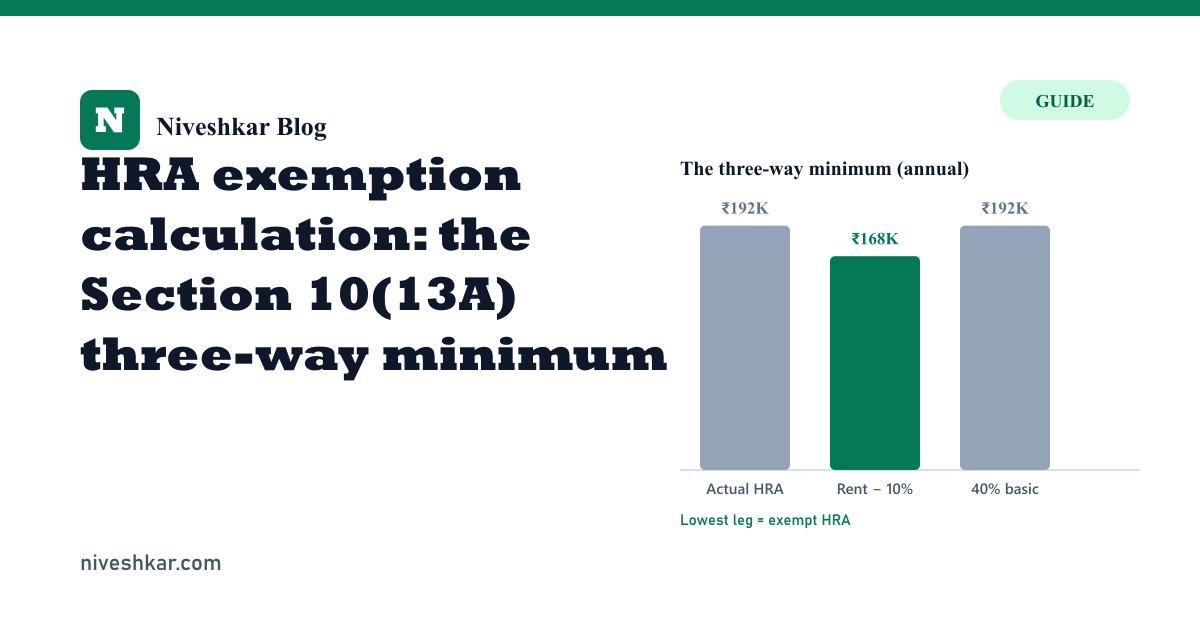

Worked example: Bengaluru, where the rent leg bites

Same exercise, non-metro this time. Monthly basic ₹40,000, HRA ₹16,000, rent ₹18,000, in Bengaluru.

Actual HRA: ₹1,92,000. Rent for the year is ₹2,16,000, minus 10% of the ₹4,80,000 basic (₹48,000), so ₹1,68,000. Non-metro leg: 40% of ₹4,80,000, so ₹1,92,000.

Legs are ₹1,92,000, ₹1,68,000 and ₹1,92,000. The lowest is ₹1,68,000, set by the rent leg. So ₹1,68,000 is exempt and the remaining ₹24,000 of HRA is taxable. At 20.8% the exemption saves about ₹34,900, and the leftover ₹24,000 adds roughly ₹5,000 of tax back. Notice what would have happened if this person had wrongly claimed metro 50%: the leg would have been ₹2,40,000, still above the rent leg’s ₹1,68,000, so the exempt figure wouldn’t have moved at all. The metro error buys nothing here and risks a query. That’s the pattern, more often than not.

Paying rent to your parents

This works, and it’s legal, and the tribunals have backed it many times. But only when it’s real. The house has to be owned by your parent, not by you. The rent has to actually leave your account and reach theirs, every month, ideally by bank transfer so there’s a trail. And your parent declares that rent as income in their own return. If they’re below the taxable threshold or sit in a lower slab, the family keeps more money overall while you claim a legitimate HRA exemption.

Where it falls apart is when people treat it as paperwork. No money moving. No rent agreement. A parent who never shows the income. Rent that happens to equal the exact HRA cap to the rupee. That fact pattern gets struck down on scrutiny and the exemption is reversed with interest tacked on. I’d say it’s one of the cleaner tax moves available to a salaried renter whose parents own their home, as long as you run it like a real tenancy. Pay by transfer, keep an agreement, make your parent report it. Cash-in-an-envelope arrangements are not worth the risk.

HRA without a rent receipt

For rent up to ₹3,000 a month, most employers will process the HRA claim without receipts. Above that, you need them. The bigger trigger is annual: the moment your rent for the year crosses ₹1,00,000, which is about ₹8,333 a month, you have to report your landlord’s PAN to your employer. No PAN, and the exemption can be denied at the TDS stage and questioned when you file.

Keep the paperwork even when you’re sure you won’t need it. A rent agreement, monthly receipts, and bank-transfer proof cover you fully. The one situation that genuinely bites is a landlord who refuses to share a PAN while your rent is over ₹1 lakh a year, because the law puts that disclosure squarely on you, not on them. If you’re house-hunting and weighing rent against buying, the EMI calculator handles the other side of that decision.

HRA under the new tax regime

It’s gone. The new regime under Section 115BAC switches off the HRA exemption along with 80C, Section 24(b) home loan interest and nearly every other deduction. Choose the new regime and your entire HRA is taxable. So this whole calculation only matters if you’re on the old regime.

And this is exactly why the regime choice isn’t automatic for renters. For someone in Mumbai or Delhi paying ₹40,000-plus in rent, the HRA exemption can be shielding ₹3 to ₹4 lakh a year. Throw that away by moving to the new regime, and the lower new-regime rates often don’t claw the gap back. I won’t tell you which regime wins, because it genuinely depends on your numbers. What I’ll tell you is to stop assuming the new regime is automatically better just because it’s the default and everyone keeps talking about it. Run both. The income tax calculator does the side-by-side, and the old vs new regime guide walks through the income bands where each one comes out ahead.

Section 80GG vs 10(13A): the self-employed route

The difference between Section 80GG and Section 10(13A) is simply who gets which. 10(13A) is for salaried people who receive an HRA component; 80GG is for everyone who pays rent but gets no HRA, including the self-employed. You can never claim both for the same period. 80GG is the far weaker of the two, capped at ₹60,000 a year against HRA’s uncapped three-way minimum, so if you have any HRA in your salary you want 10(13A), not 80GG.

No HRA in your salary, or no salary at all because you’re self-employed? Then 10(13A) doesn’t apply to you, but you’re not entirely shut out. Section 80GG gives a rent deduction to people who pay rent and get no HRA. It’s the least of three figures: ₹5,000 a month, 25% of total income, or rent minus 10% of total income. It caps out at a miserly ₹60,000 a year, far less than a real HRA exemption, but it’s something. You also can’t own a home in the same city, and you have to file Form 10BA to claim it. For freelancers and consultants paying genuine rent, it’s worth the small effort.

What I’d actually do

Three habits save the most money here. First, learn the four-city metro list and stop guessing. Second, look at the rent leg before you assume your HRA is fully exempt, because it usually isn’t. Third, if your parents own the home you’d otherwise rent in the open market, pay them rent properly and claim the exemption, because that’s real money staying in the family rather than going to the government.

The thing nobody tells you is that HRA is a bigger lever in the regime decision than 80C ever was. 80C tops out at ₹1.5 lakh. A metro renter’s HRA exemption can be double or triple that. So if you’re a renter staring at the old-versus-new question, the HRA number is probably the one doing the deciding. Compute it first, then choose.