Step-up SIP: how it works + the ₹2 crore math over 25 years

Step-up SIP math: a 10% annual increase roughly doubles a 25-year corpus vs a flat SIP. The cashflow plan that keeps it running, mistakes that halve it.

Picture two SIPs, both started in 2001 at ₹3,000 a month. Same fund, same expected return, same investor risk tolerance. Twenty-five years later, one finishes at about ₹57 lakh. The other finishes at about ₹1.16 crore. The difference isn’t the fund manager, the market, or luck. The first investor never raised the SIP. The second raised it 10% every year on the SIP anniversary. That’s the whole gap.

Most Indian investors are the first one. They set up a SIP in their late twenties when ₹10,000 a month was a stretch, and then they let it run untouched for twenty years while their salary roughly quintuples. The SIP becomes a footnote on the bank statement. Inflation does the rest of the destruction. By year 20, what felt like serious investing in year 1 has become rounding error.

A step-up SIP fixes this in one setting. Two numbers instead of one: the starting monthly and the annual step-up percentage. The platform handles the rest.

What the step-up does mechanically

A flat SIP is the same monthly amount forever. A step-up SIP raises the monthly contribution every year on the same calendar date, usually the SIP anniversary. At 10% step-up, ₹10,000 in year 1 becomes ₹11,000 in year 2, ₹12,100 in year 3, ₹13,310 in year 4. Year 25 hits ₹98,497. Total contribution: ₹1.18 crore. The NACH mandate refreshes automatically each year without any manual action from you.

Every major mutual fund platform in India supports this natively. Groww, Zerodha Coin, Kuvera, Paytm Money, ETMoney and the AMC direct platforms (HDFC, ICICI, SBI, Axis, Kotak) let you set the step-up percentage when you create the mandate. The annual bump happens automatically through the NACH refresh. The step-up amount caps at whatever the NACH transaction limit on your bank account is, typically ₹1 lakh per transaction for personal accounts.

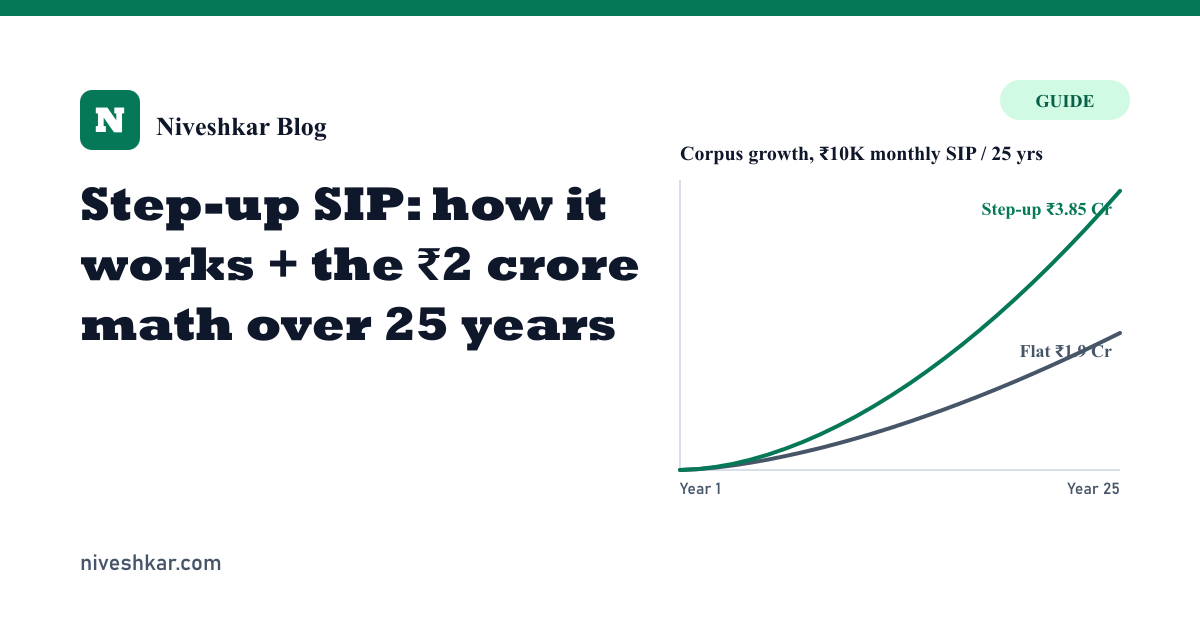

The numbers, side by side

Two ₹10,000 starting SIPs, both 25 years, both at the same realistic 12% expected return (post-expense long-run return on broad equity in India).

Flat SIP: ₹10,000 a month for 300 months. Total contribution ₹30 lakh. Corpus at 12%: about ₹1.89 crore.

Step-up SIP at 10%: ₹10,000 starting, ₹98,497 at the end. Total contribution about ₹1.18 crore. Corpus at 12%: about ₹3.85 crore.

The step-up version invests 4x the rupees and ends with about 2x the corpus. That ratio is the give-away. The step-up doesn’t create alpha. It just stops inflation from eating your contribution while only the corpus benefits from compounding.

Drop the expected return to a more conservative 11% and the gap holds: flat ends at ₹1.69 crore, step-up at ₹3.34 crore. At 10% return, flat is ₹1.50 crore and step-up is ₹2.90 crore. The ratio is sticky across realistic return assumptions because the leverage is on the contribution path, not on the return.

Punch your own starting amount and step-up rate into the SIP calculator. Set step-up to zero to see the flat baseline. Bump it to 10% and you’ll see the gap I’m describing here.

Why 10% is the right number

Three reasons converge on roughly 10%.

Average salary growth for salaried professionals in India runs 8% to 12% in the first decade of a career, slowing to 5-7% in the second. A 10% step-up roughly tracks this, so the SIP keeps the same share of net pay throughout your working life. You don’t notice the increase because your salary is increasing alongside.

Long-run inflation under RBI’s 4% (±2%) target band lands around 5-6%. A 10% nominal step-up keeps the real (inflation-adjusted) contribution growing at 4-5% a year. That’s actual additional purchasing power going into the SIP, not just keeping pace.

NACH mandate limits at most retail banks comfortably accommodate even the year-25 contribution of about ₹1 lakh, so you don’t have to renegotiate the mandate mid-tenure.

A 5% step-up is too soft. The contribution barely tracks inflation, so in real terms you’re running a flat SIP again. A 15% step-up looks great on paper but few Indian professionals actually see consistent 15% salary growth across 25 years, and by year 12-13 the SIP starts crowding out other cashflow priorities. People pause it. Once a SIP is paused, the discipline rarely fully recovers.

10% is the sweet spot. Set it, automate it, forget it.

The cashflow trap

This is where most step-up plans die.

The math works only if the SIP actually runs uninterrupted for 25 years. The most common failure mode: the step-up triggers in a year when the increment was smaller than expected, or rent went up by more, or a wedding happened, and the SIP starts quietly eating into discretionary spend that wasn’t budgeted for the cut. The NACH still goes through. The credit card balance creeps up to compensate. Net wealth: flat.

Three habits keep this alive.

Start lower than you think you should. If you can comfortably set up ₹15,000 a month today on a flat SIP, run ₹12,000 a month on a step-up instead. The lower starting buys you margin for the year-1 and year-2 increases without scrambling. By year 5, both versions converge in monthly outflow, but the step-up version is already compounding harder.

Tag the SIP date to one day after your salary credit, not the 1st of the month. The contribution clears before any discretionary spending starts. People who set their SIP date as the 5th or 10th end up “managing” the SIP around month-end pressure, which is exactly the wrong way around.

Treat the annual step-up as a salary-day event, not a SIP event. Anchor it to April or whenever your appraisal letter usually lands. The step-up should feel like an automatic claim on the raise you just got, not a surprise tightening of cashflow three months later.

Fund proliferation, the other killer

People run three separate ₹3,000 step-up SIPs into three different equity funds because they read somewhere that diversification helps. After 10 years there’s no meaningful diversification left, just three sets of NAV statements, three tax events on redemption, and a portfolio that’s mostly the same large-cap stocks held three times over through different fund houses.

One step-up SIP into one well-chosen large-and-mid-cap or flexi-cap fund covers the same ground with less friction. Diversify across asset classes (equity, PPF, FD, real estate), not across funds inside the same equity category. The latter is just confusion at scale.

If you have three funds running from a decade ago, don’t redeem to consolidate. That triggers LTCG. Stop fresh SIPs into two of them. Let the existing balances compound. Direct new step-up SIPs into your one chosen fund. Over the next decade, the portfolio naturally rebalances around the active fund.

What pauses actually cost

Real life is messier than spreadsheets. Job change, business loss, medical event, marriage, child. All reasons to pause or reduce the SIP. The good news: short pauses don’t break the math.

A 24-month pause in year 10 of a 25-year ₹10,000 step-up SIP costs about ₹35 lakh of final corpus. On an expected ₹3.85 crore endpoint, that’s roughly a 9% loss. Painful but not catastrophic.

A 60-month pause in the same year costs about ₹85 lakh, or 22%. Now you’re looking at meaningful damage.

The middle years (8-15) carry the most weight because both the contribution amount and the remaining compounding window are large at the same time. Pauses in year 1-3 are cheap. Pauses in year 20-25 are also cheap. The expensive ones are years 8-15.

If you have to pause, don’t stop the SIP entirely. Drop it to the minimum allowed (₹500 at most platforms) rather than cancelling. Keeps the mandate alive, keeps the step-up clock running, lets you resume the originally-planned monthly amount when cashflow recovers. Restarting a cancelled SIP often resets the step-up schedule, and the platform may not let you back-date the trajectory you originally locked in.

The tax bit nobody tells you about

A step-up SIP that ends at ₹98,000 monthly in year 25 means the bulk of your investing happens in the last 10 years of the plan, not the first. This matters when you eventually redeem.

Under the current Section 112A regime, LTCG above ₹1.25 lakh per financial year on equity mutual funds is taxed at 12.5% (post the July 2024 budget change). A ₹3.85 crore corpus with most of the gains accruing in the last decade means a single-shot redemption would trigger a substantial tax bill on the full gain.

Plan the redemption as a 5-7 year staggered withdrawal starting two years before retirement, not as a single transfer. The free ₹1.25 lakh annual LTCG exemption used across 6-7 years can shield ₹8-9 lakh of gains from tax. On a ₹2 crore gain expected from a 25-year step-up SIP, that’s roughly ₹1.1 lakh of tax saved with no risk and no asset-allocation change. Pure execution win.

The other side of the coin: don’t tinker with the step-up rate every 3 years to “optimise” against recent fund performance. That’s the textbook way to underperform a passive plan. Set it, leave it, ignore it.

The bet I’d take

If I had to pick the single most under-used personal-finance lever in India right now, it would be this one. The 25-year flat-vs-step-up gap of roughly ₹2 crore at a ₹10,000 starting monthly is one of the biggest leverage points available to a salaried investor who is not changing asset allocation, not picking stocks, and not paying for advice. Pure decision-once, automate-forever.

Punch your own salary growth assumption and starting SIP amount into the SIP calculator before the next NACH mandate refresh. Set the step-up. Forget it. Re-check the corpus when your tenth wedding invitation lands, twelve years from now. You’ll find it’s gone somewhere unfamiliar.