NPS Tier-1 vs equity mutual funds: which builds the better retirement?

NPS vs equity mutual funds for retirement: the 80CCD(1B) deduction, the forced 40% annuity, tax at every stage, and why most people should use both.

Every December a colleague forwards me the same WhatsApp message: “Invest ₹50,000 in NPS before March 31, save ₹15,600 in tax.” It’s true, as far as it goes. What the message never says is that you’ve just locked that ₹50,000 away until you’re 60, and that a chunk of what it eventually becomes will be force-converted into a taxable pension you can’t refuse. NPS is a genuinely good product wrapped in a genuinely misleading pitch. The honest question isn’t “NPS or mutual funds” — it’s “what is each one actually for”, and the answer for most people is “both, in a specific ratio”.

Here’s the whole debate in one line. NPS is cheaper, gives you an exclusive ₹50,000 tax deduction, and forces you to stay invested, but it caps your equity and makes you annuitise 40% into a low-yield, slab-taxed pension. An equity mutual fund SIP has no cap, full liquidity and friendlier capital-gains tax, but no extra deduction and no discipline baked in. Run both through the NPS calculator and the SIP calculator and the numbers tell the rest of the story.

What you’re actually comparing

NPS Tier-1 is a retirement account. You contribute monthly, a pension fund manager invests it across equity, corporate bonds and government securities at a fund-management charge of about 0.09% — the cheapest managed product in India by a wide margin. It’s locked until 60. At exit you take up to 60% as a tax-free lump sum and must use at least 40% to buy an annuity that pays a monthly pension for life.

An equity mutual fund SIP is just a fund. You pick it, set a monthly auto-debit, and it buys units at the day’s NAV. A direct-plan equity fund runs at 0.5-1.2% a year, more than NPS but still cheap. There’s no lock-in (outside ELSS), no equity cap, and no forced annuity. You decide when and how much to withdraw.

So the products differ on four axes that actually matter: cost, tax, flexibility, and discipline. NPS wins two of them cleanly and loses two.

Round 1: cost and returns

NPS wins on cost, full stop. The 0.09% fund-management charge versus 0.5-1.2% for an active equity fund sounds trivial until you compound it over 30 years, where it works out to a corpus 10-15% larger for the same gross return. Even against a direct index fund at 0.2%, NPS is marginally cheaper.

But NPS caps equity at 75% until age 50, then tapers it down. A young investor in a pure equity mutual fund can run 100% equity for decades. Over a 30-year horizon that higher equity share usually more than offsets NPS’s cost advantage, because equity’s long-run return premium over the bond portion of an NPS fund is larger than the fee gap. The net effect: in the accumulation phase, a 100% equity SIP typically edges out a 75%-equity NPS on gross corpus, and the gap widens the longer the horizon. NPS’s cost edge is real but not decisive.

Round 2: tax, which is where it gets complicated

This is the round everyone gets wrong, because NPS is taxed at three separate points and people only remember the nice ones.

Going in, NPS is excellent. Your contribution is deductible under Section 80CCD(1) within the ₹1.5 lakh 80C ceiling, plus an exclusive extra ₹50,000 under Section 80CCD(1B) that nothing else can claim, plus employer contributions up to 10% of salary under Section 80CCD(2). That 80CCD(1B) ₹50,000 is the single best reason to hold NPS — at the 31.2% slab it’s ₹15,600 of tax saved every year, on money you were going to save anyway. A mutual fund SIP gives you no deduction at all (ELSS is the exception, but that’s a different ₹1.5 lakh under 80C, available only in the old regime).

At 60, the 60% lump sum is fully tax-free under Section 10(12A). So far NPS is winning the tax round comfortably.

Then the annuity ruins the scorecard. The mandatory 40% buys a pension that is added to your income and taxed at your slab rate, every single year, for the rest of your life. Compare that to an equity mutual fund, where withdrawals are long-term capital gains taxed at 12.5% above ₹1.25 lakh a year — and you control the timing, so you can spread redemptions to use the exemption each year. A retiree drawing income from equity funds is often taxed more lightly than one drawing the same income from an NPS annuity.

So the tax verdict is split: NPS wins decisively on the way in and on the lump sum, and loses on the pension. The deduction is upfront and certain; the annuity tax drag is spread over decades. For most people the upfront ₹50,000 deduction is worth more in present-value terms than the eventual annuity tax costs — for the first ₹50,000 a year. Beyond that, the calculus shifts toward mutual funds.

Round 3: flexibility and the forced annuity

This is where NPS pays for its discipline. The 40% annuitisation is not optional, and annuity rates in India are low — currently around 6-7% — and the income is fully taxable. You’re handing four-tenths of a corpus you spent 30 years building to an insurer in exchange for a modest, taxable, often non-inflation-adjusted pension. For many people, drawing down an equity-and-debt portfolio yourself via an SWP would produce more income with more control and a smaller tax bill.

Premature exit is worse. Leave NPS before 60 and you must annuitise 80%, leaving just 20% as a lump sum. Partial withdrawals are allowed — 25% of your own contributions, after three years, for specific needs — but the account is designed to be illiquid. A mutual fund, by contrast, is liquid to a fault, which is both its strength and its trap: the same freedom that lets you handle an emergency also lets you panic-sell in a crash.

That illiquidity is the hidden feature. The behavioural value of an account you literally cannot touch until 60 is real, and it’s the strongest non-tax argument for NPS. Plenty of people who would have churned a mutual fund portfolio into mediocrity will leave an NPS account alone simply because they have no choice.

The numbers, side by side

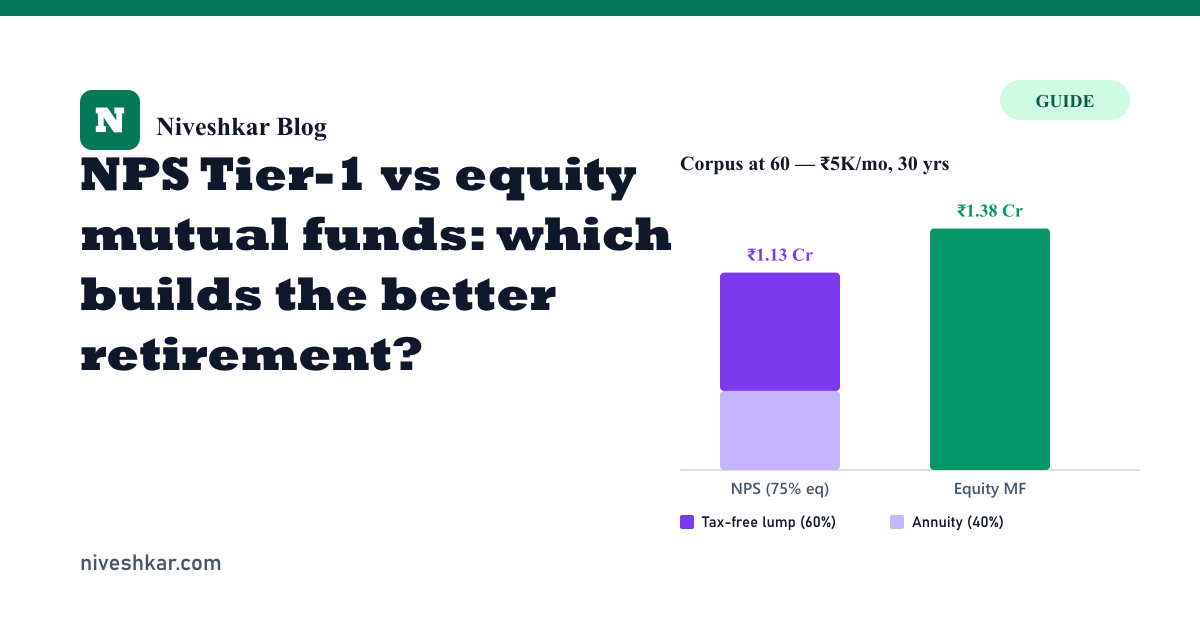

Take a 30-year-old putting ₹5,000 a month away for 30 years at 10%. The NPS corpus comes to roughly ₹1.14 crore. Annuitise the minimum 40% (₹45.6 lakh) at 6% and the pension is about ₹22,800 a month, taxable; the 60% lump sum (₹68.4 lakh) is tax-free. Plug your own figures into the NPS calculator to see the split.

The same ₹5,000 a month into a 100% equity fund at, say, 11% (the higher equity share earns a bit more) builds a larger corpus, all of it liquid, taxed at 12.5% LTCG only when you sell, with no forced annuity. But you got no ₹50,000 deduction along the way, and nothing stopped you from raiding it at 45 for a car.

Neither number is “the answer”, because they’re not the same product. One is a disciplined, tax-advantaged, semi-liquid pension. The other is a flexible, lightly-taxed, fully-liquid corpus you have to manage yourself.

What most people should actually do

Use both, in this order:

- Contribute ₹50,000 a year to NPS Tier-1 purely to capture the 80CCD(1B) deduction. This is close to free money if you’re in the old regime and paying tax at 20% or 30%. The annuity drag on this slice is small relative to the upfront saving.

- Route the rest of your retirement saving into direct-plan equity mutual fund SIPs, where it stays liquid, stays in your control, and is taxed more kindly on the way out.

- If you’re on the new tax regime, the maths changes — 80CCD(1B) and 80CCD(1) don’t apply, only the employer-contribution 80CCD(2) survives. Without the deduction, NPS loses much of its edge for individual contributions, and equity funds become the cleaner default. Check which regime you’re on with the income tax calculator before deciding.

The WhatsApp forward isn’t wrong that NPS saves tax. It’s just answering a smaller question than the one you should be asking. NPS is an excellent ₹50,000-a-year tax-advantaged pension sleeve and a mediocre place to put your entire retirement. Size it accordingly, let equity mutual funds do the heavy lifting, and you get the deduction without surrendering control of the whole corpus.