Home loan vs SIP: should you prepay or invest the surplus?

Home loan vs SIP: post-tax loan cost after Section 24 vs post-tax SIP return, worked at 3 salary slabs and the income where math flips.

The standard advice on Reddit, YouTube and every other personal finance YouTuber’s thumbnail is “always invest, never prepay”. Equity returns 12%, home loans cost 9%, what’s there to think about?

There’s a lot to think about. The 12% is pre-tax pre-expense pre-LTCG. The 9% is the headline rate before Section 24(b) and slab rate do their work. After both adjustments, the gap shrinks and sometimes flips. The popular take ignores the math that decides the answer. Run it properly and prepay wins below ₹15 lakh CTC, equity SIP wins above ₹40 lakh, and the band in the middle depends on whether you have an active home loan in its first decade.

This piece walks through the post-tax arithmetic at three real salary points so you can find your number.

What the loan actually costs you, post-tax

A 9% home loan is not a 9% liability for someone claiming Section 24(b). Up to ₹2 lakh of home loan interest per financial year on a self-occupied property is deductible under the old regime. The tax saved equals the deducted interest multiplied by your marginal slab plus 4% cess.

Numbers help. A 30% slab borrower (31.2% including cess) claiming the full ₹2 lakh interest deduction saves ₹62,400 in tax per year. On a ₹50 lakh home loan at 9%, year-1 interest is about ₹4.42 lakh. The tax shield reduces effective interest from ₹4.42L to ₹3.80L, which is an effective post-tax loan rate of about 7.6%.

Same loan, 20% slab borrower (20.8% with cess). The ₹2L deduction saves ₹41,600 of tax, effective rate climbs to about 8.2%.

5% slab borrower (5.2% with cess). Tax shield only ₹10,400, effective rate is about 8.8%, basically the headline rate.

The Section 24(b) cap kicks in early. As the outstanding balance falls and annual interest drops below ₹2 lakh (typically around year 8-10 of a 20-year loan), the shield starts shrinking proportionally to the actual interest paid. By year 15, the effective post-tax rate has crept back up close to the headline 9%.

One important asterisk. The new tax regime kills Section 24(b) entirely for self-occupied property. If you’ve already switched to the new regime, your home loan is at the full headline rate from day one, and the math in this piece changes substantially in favour of prepayment. I’m running everything below assuming old regime; reverse the conclusion if you’re on new.

What the equity SIP actually returns, post-tax

A 12% expected return from a broad equity mutual fund is the pre-tax, pre-expense, pre-LTCG figure on the factsheet. Three deductions before the rupee reaches your account.

Direct-plan flexi-cap expense ratio runs around 0.5-0.8% annually. After expense, the realised return is roughly 11.2-11.5%.

On redemption, LTCG above ₹1.25 lakh per financial year is taxed at 12.5% under Section 112A as updated in July 2024. The exact post-tax annualised return depends on the redemption sequence, but for a multi-year SIP redeemed across a sensible 5-7 year window, the effective post-tax post-expense post-LTCG return lands around 10.2-10.5%.

This is the comparator. Not 12%. Not 11%. Roughly 10.3% post-everything, assuming the equity market actually delivers its long-run historical return and you stagger the redemption intelligently across financial years.

Three things kill the 10.3% number for many investors. Switching funds every two years to chase last year’s winner (chargeable LTCG each time, hidden 1-2% drag). Panic-redeeming during a 30%+ drawdown and staying out (the post-tax return drops to 5-6% if you actually behave this way). Holding regular-plan instead of direct-plan funds (extra 0.7% expense compounded over 15 years is roughly ₹15-20 lakh on a ₹2 crore corpus). Fix those and the 10.3% is realistic.

Worked example: ₹12 lakh CTC, 5% slab, year-3 of home loan

Outstanding balance ₹40 lakh at 8.5%, remaining tenure 17 years. Year-3 interest about ₹3.30 lakh, but only ₹2 lakh is deductible under Section 24(b). Effective post-tax loan rate: ₹2L deductible × 5.2% slab = ₹10,400 saved on ₹3.3L paid, effective rate roughly 8.2%. Monthly surplus available: ₹5,000.

Prepayment route. ₹5,000 a month for the next 17 years totals ₹10.2 lakh of extra principal payments. Net interest saved over the remaining tenure: about ₹14.8 lakh. Tenure shrinks by 4 years and 3 months. Final EMI stops 4 years earlier.

Equity SIP route. ₹5,000 step-up SIP at 10% annual increase, 17-year horizon, 10.3% post-tax return. Final corpus: about ₹35 lakh. Cumulative contribution: about ₹25 lakh.

The SIP looks dramatic in absolute rupees. But the prepay benefit is locked in cash that never leaves the household, while the SIP corpus is subject to equity drawdowns and behavioural risk. The 8.2% certain return from prepayment, combined with the psychological benefit of finishing the loan early, beats the 10.3% expected-but-variable equity return at this slab. Prepay.

This is the income band where most personal finance influencers give the worst advice. “Always invest” works for them because their audience skews ₹40 lakh+. For a ₹12 lakh CTC household with a home loan, the certain interest saving usually beats the variable equity return.

Worked example: ₹25 lakh CTC, 20% slab, year-5 of home loan

Outstanding ₹55 lakh at 8.75%, remaining 15 years. Year-5 interest about ₹4.6 lakh, capped at ₹2L for the deduction. Effective post-tax rate: ₹2L × 20.8% = ₹41,600 saved on ₹4.6L paid, effective rate roughly 7.9%. Monthly surplus: ₹15,000.

Prepay route. ₹15,000 monthly part-prepayment for 15 years saves about ₹38 lakh of interest. Tenure shrinks by 5 years 4 months.

Equity SIP route. ₹15,000 step-up SIP at 10%, 15 years, 10.3% post-tax. Final corpus: about ₹86 lakh.

Closer call than the absolute numbers suggest. Post-tax loan rate 7.9% versus post-tax equity return 10.3%. That’s a 2.4 percentage point gap. Compounded over 15 years on ₹15K monthly, it becomes a roughly ₹48 lakh difference in favour of the SIP. But the SIP rides the equity volatility for the whole tenure. If you’re the kind of investor who actually holds through a 35% drawdown without exiting, take the SIP. If you’ve never sat through one and you’re guessing at your reaction, hedge.

The hedge: split the surplus 60/40 between part-prepayment and SIP. ₹9,000 to prepay, ₹6,000 to SIP. You get certain interest saving on the bigger chunk and equity upside on the smaller one. Mixed strategy is usually correct in this band.

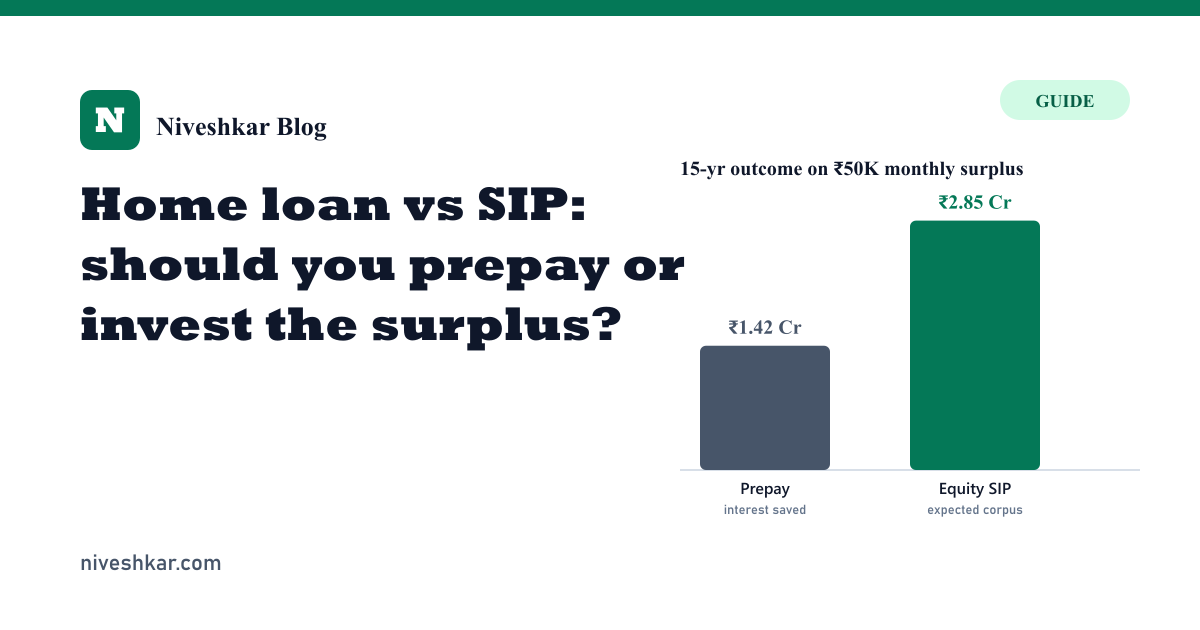

Worked example: ₹50 lakh CTC, 30% slab, year-5 of home loan

Outstanding ₹85 lakh at 8.75%, remaining 15 years. Year-5 interest ₹7.1 lakh, capped at ₹2L. Effective rate: ₹2L × 31.2% = ₹62,400 saved on ₹7.1L paid, effective rate 7.9%. (Same effective rate as the previous example because as absolute interest grows, the cap shrinks the shield proportion.) Monthly surplus: ₹50,000.

Prepay route. ₹50,000 monthly prepayment saves about ₹1.42 crore of interest over 15 years. Tenure shrinks by 6 years 8 months.

Equity SIP route. ₹50,000 step-up SIP at 10%, 15 years, 10.3% post-tax. Final corpus: about ₹2.85 crore.

Now equity SIP starts winning meaningfully. The 2.4 percentage point gap compounded on ₹50K monthly over 15 years works out to roughly ₹1.4 crore of advantage. The certainty premium that justified prepay at lower incomes is less valuable at this slab because the household already has other certainty buckets sitting around (EPF, PPF, FDs, the existing home equity, NPS Tier-1). One more certainty bucket is diminishing returns. The variance bucket is what’s actually missing. Equity SIP wins, with caveats.

The caveats: the same household with the home loan in year 12+, where the Section 24(b) shield has mostly worn off and the post-tax loan rate is creeping back to 9%, should reverse the conclusion. The gap closes when the shield closes.

When prepay actually wins, even at high incomes

Four triggers in rough order of importance.

Less than 8 years remaining on the loan. The Section 24(b) shield has mostly evaporated by then, the effective rate is climbing back to the headline, and the equity compounding window is too short to absorb a serious drawdown without breaking the original plan. Below 8 years, prepay regardless of slab.

You’re on the new tax regime for self-occupied property. No 24(b), so the effective loan rate equals headline. A 9% certain saving beats a 10.3% expected-but-variable return in any realistic utility calculation.

Let-out property with sub-3.5% rental yield. The post-tax economics of holding the property are uglier than they look, and reducing principal accelerates the eventual exit if you want to sell.

You’d panic during a 30%+ equity drawdown and redeem at the wrong time. The 10.3% expected return assumes you hold through the cycle. If your real behaviour is partial exits at lows, your realised return drops to 5-6% and prepay beats SIP comfortably. Most people overestimate their tolerance for volatility until they actually experience it. Be honest about which type you are.

When equity SIP wins, even at moderate incomes

You’re in the 30% slab and the loan is in years 1-7 with the full 24(b) shield. Effective post-tax rate around 7.6%, gap to equity widens, multi-decade compounding window. Tilt heavily toward SIP.

You don’t currently hold any equity in the household portfolio. Prepay reduces a known liability but doesn’t build an asset class you’re missing. Build the equity exposure first; once it’s there, you can decide between adding to it or prepaying the loan.

You strongly expect RBI to ease over the next 3-5 years. Current 8.5-9% rates are at the upper end of the post-COVID range. If repo eases and home loan rates drift to 7.5%, the math tilts harder toward equity SIP. (Caveat: don’t bet the house on rate predictions. If they materialise, great. If not, your decision was right on current rates anyway.)

The hybrid is usually the answer

For the ₹15-30 lakh CTC band, a clean 60/40 split between part-prepayment and a step-up SIP works for most households. The prepayment shrinks a known liability and gives a psychological win every year. The SIP builds an equity bucket that doesn’t depend on the loan schedule. After year 8 of the loan, shift the split to 30/70 in favour of SIP because the 24(b) shield is shrinking and the equity compounding window is still long.

Run your own numbers in the EMI calculator for the prepay side and the SIP calculator for the equity side. Change the slab, the tenure, the step-up rate. Stress-test against a 30% equity drawdown by running the SIP at 8% return instead of 10.3% and see how the answer shifts.

The default advice of “always invest” is wrong for anyone below ₹15 lakh CTC. “Always prepay” is wrong for anyone above ₹40 lakh in the 30% slab with a fresh loan. The right answer for you lives somewhere on that spectrum, and the only way to find it is to put your actual numbers in the calculators and watch the math decide.