Capital gains tax after July 2024: what actually changed and who pays more

The 23 July 2024 capital gains overhaul, explained: 12.5% LTCG, the ₹1.25 lakh equity exemption, 20% equity STCG, and the property indexation trade-off.

The July 2024 budget did something rare: it changed capital gains tax for almost everyone at once, and it did it mid-year, so a single financial year now has two sets of rules split at 23 July 2024. Most of the explainers floating around still quote the old numbers — 10% LTCG, a ₹1 lakh exemption, indexation on property. If you’re selling anything this year, those are wrong, and the gap can be tens of thousands of rupees. Here is what actually changed, who comes out ahead, and who quietly pays more. Run your own numbers through the capital gains calculator alongside.

The one-paragraph summary

Long-term equity gains went from 10% to 12.5%, but the annual exemption rose from ₹1 lakh to ₹1.25 lakh. Short-term equity went from 15% to 20%. For property, gold and other long-term assets, the rate dropped to a flat 12.5%, but indexation was abolished — with a grandfathering escape hatch for property bought before the cut-off. Debt funds were already slab-taxed since April 2023 and didn’t change. That’s the whole reform. The rest is working out which side of each line you’re on.

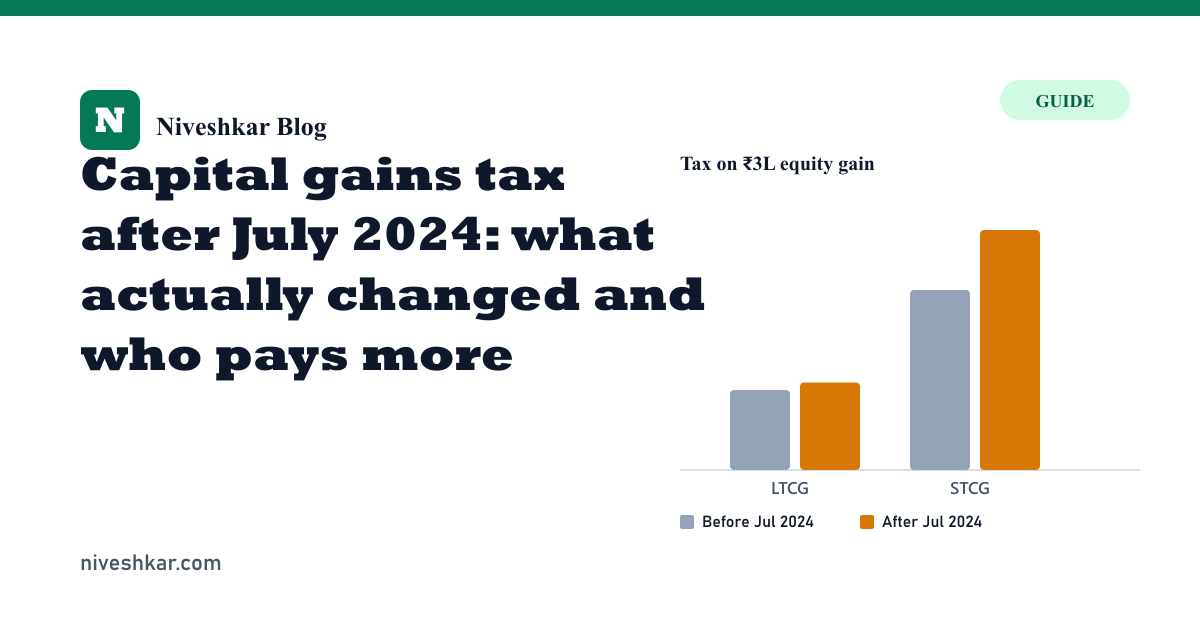

Equity: a small rise, dressed up as a giveaway

For listed shares and equity mutual funds, the headline is that long-term capital gains tax rose from 10% to 12.5%. The government softened the optics by lifting the tax-free slice from ₹1 lakh to ₹1.25 lakh a year. For small investors with modest annual gains, the higher exemption genuinely offsets the rate hike. For anyone realising more than about ₹8 lakh of long-term gains in a year, the 2.5-point rate increase dominates and you pay more.

Short-term equity is the part nobody advertises. The rate jumped from 15% to 20% — a third higher — with no exemption at all. If you trade or churn equity funds inside 12 months, this is a real, immediate increase. The reform’s clear message is: hold equity longer than a year, and don’t trade.

The planning lever that still works is the financial-year reset. The ₹1.25 lakh exemption is per year, so splitting a large redemption across 31 March shelters ₹2.5 lakh of gains instead of ₹1.25 lakh. If you build wealth through SIPs, remember each installment has its own purchase date for the 12-month test — the SIP calculator shows how the corpus stacks up before you plan the exit.

Property: the indexation trade-off

Property is the genuinely contentious change. The long-term rate fell from 20% to 12.5%, which sounds like a cut — until you notice indexation was removed. Indexation used to inflate your purchase cost by the Cost Inflation Index, shrinking the taxable gain to reflect that a rupee in 2005 isn’t a rupee today. Without it, your “gain” is the full nominal difference, including decades of inflation.

After an outcry, the government added a grandfathering rule. For property and land bought before 23 July 2024, you can choose the lower of two routes: 12.5% without indexation, or 20% with indexation. For property bought on or after that date, only the flat 12.5% applies and indexation is gone for good.

Which route wins depends on holding period and price growth:

- Long holding, modest appreciation → the indexed 20% route usually wins, because indexation eats most of the nominal gain. A flat held 18 years where prices merely kept pace with inflation could owe almost nothing under indexation but a hefty 12.5% on the full nominal gain without it.

- Short holding or strong appreciation → the flat 12.5% usually wins, because there’s been little inflation to index away and the lower rate dominates.

The only way to know is to compute both. The capital gains calculator takes an indexed cost and pays you the lower of the two automatically. Get the Cost Inflation Index for the relevant years from the income tax department — FY 2024-25 is 363 against a 2001-02 base of 100.

Debt funds and gold

Debt mutual funds didn’t change in July 2024 because they’d already been gutted in April 2023. Units bought on or after 1 April 2023 are taxed at your slab rate on the entire gain under Section 50AA — no long-term concession, no indexation, regardless of holding period. This is why debt funds lost their edge over fixed deposits for most savers; the FD calculator gives you the guaranteed-return comparison.

Gold, gold funds, unlisted shares and most other assets follow the new long-term rule: 12.5% without indexation if held over 24 months, slab rate if sold sooner. The 24-month long-term threshold matters here — equity gets long-term status at 12 months, but everything else needs 24.

Who pays more, who pays less

Putting it together:

- Small equity investors (under ~₹8 lakh annual long-term gains): roughly neutral to slightly better, thanks to the higher exemption.

- Large equity investors and traders: pay more — 12.5% vs 10% on big long-term gains, 20% vs 15% on short-term.

- Recent property buyers: pay at the flat 12.5%, generally better than the old 20% unless they’d have had heavy indexation.

- Long-term property holders (pre-July-2024): usually protected by the grandfathered 20%-with-indexation option, but must actively choose it.

- Debt fund holders: unchanged, still slab-taxed and unattractive on tax.

The mistakes I keep seeing

The most common error is applying old rates to a current sale. Any sale on or after 23 July 2024 uses the new table; a sale before it uses the old one. In a return covering both, you genuinely split the year.

The second is assuming the ₹1.25 lakh exemption applies to everything. It does not — it is exclusively for listed equity and equity mutual funds. There is no exemption on property, gold or debt gains.

The third is taking the property flat 12.5% by default. If you bought before the cut-off, not checking the indexation route can cost you real money on a long-held asset. Compute both, every time.

The last is forgetting loss set-off and the filing deadline. Short-term losses offset any capital gain; long-term losses offset only long-term gains; and the right to carry losses forward for eight years is forfeited if you file late. Net everything across the year, then fold the result into your overall liability with the income tax calculator.

The reform isn’t the disaster some headlines claimed, nor the giveaway the press releases implied. It’s a modest rate rise on equity, a real simplification-with-a-catch on property, and a nudge to hold longer and trade less. Know which line you’re on, compute both routes where you have a choice, and you won’t overpay.